Whiteboard Wednesday – Lease Accounting Standards Framework

In our 17th episode, Andy Welkley, Product Marketing Manager for MRI Software, covers a framework for lease accounting standards. With a compliance deadline for new lease accounting standards fast approaching, Andy showcases a framework for determining whether a contract classifies as a lease.

For more lease accounting standards resources, visit our resource section here: https://goo.gl/jTu1uu

Video Transcription

Andy Welkley: Hi, my name is Andy Welkley and it’s Wednesday. That means it’s time to step up to the whiteboard and talk about another issue facing real estate companies today. With a compliance deadline for the new lease accounting standards fast approaching, we’ve been spending some time talking about ways that you can prepare for these new changes. Today, we want to talk about a framework that you can use to determine whether or not a contract you have in your portfolio is a lease or not. Let’s start from the beginning.

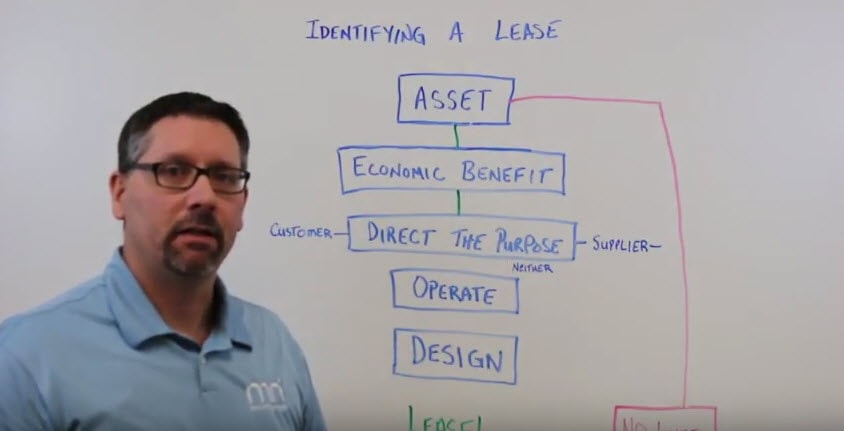

The first question we have to ask ourselves is do we have an identifiable asset? If we don’t, it’s a pretty easy decision. We don’t have a lease in most cases. However, if we are able to identify an asset, then we want to move to the next phase of our decision-making process and we want to determine whether or not we gain an economic benefit from that contract. If we do, if we gain a substantial benefit from the contract, then in all likelihood we can move to the next phase of the decision-making process.

This is where the tree begins to split a little bit. We want to ask ourselves whether the customer, you, or the supplier is the one who directs the purpose of that asset. If it’s the supplier, then again, we know that we don’t have a lease. Now, if it’s you, the customer, we can actually move down here. In all likelihood, we do have a lease. Now, it could be that neither one is the one that directs the use. It could be a predetermined use. If that’s the case we have a little more work to do.

We want to move to the next question on our list and that is can the customer, you, just operate that asset without the supplier changing those operating instructions. If that’s the case, we still have some questions to ask. We want to determine who designed that asset. If you the customer did substantially the work to design that asset or substantial aspects of that asset, then in all likelihood you have a lease. However, if that’s not the case, then you don’t have a lease and we can move to that stage.

We’ve gone fast through this process, so we’ve prepared and infographic that mirrors some of the conversation that we’ve had today. You can find that link below. If you want to dive deeper, we have a podcast as part of our building success series where we dive really deep into this concept and talk about the ways that you can prepare for this upcoming change. That’s Whiteboard Wednesday for today. My name is Andy Welkley. Thanks very much.