Whiteboard Wednesday – Resident Screening

On this week’s episode of MRI Software’s Whiteboard Wednesday series, we explore our Resident Screening software for multifamily properties. Andy Welkley, Product Marketing Manager for MRI Software, covers the nuances of risk balanced with driving occupancy. He discusses how the typical residential resident screening process works, and then contrasts it with MRI Software’s Resident Screening solution which uses proprietary algorithms and in-house private investigators to provide a more measured, accurate approach to driving occupancy.

Watch to learn how MRI’s Resident Screening software can make a meaningful difference in your resident application process.

Video Transcription

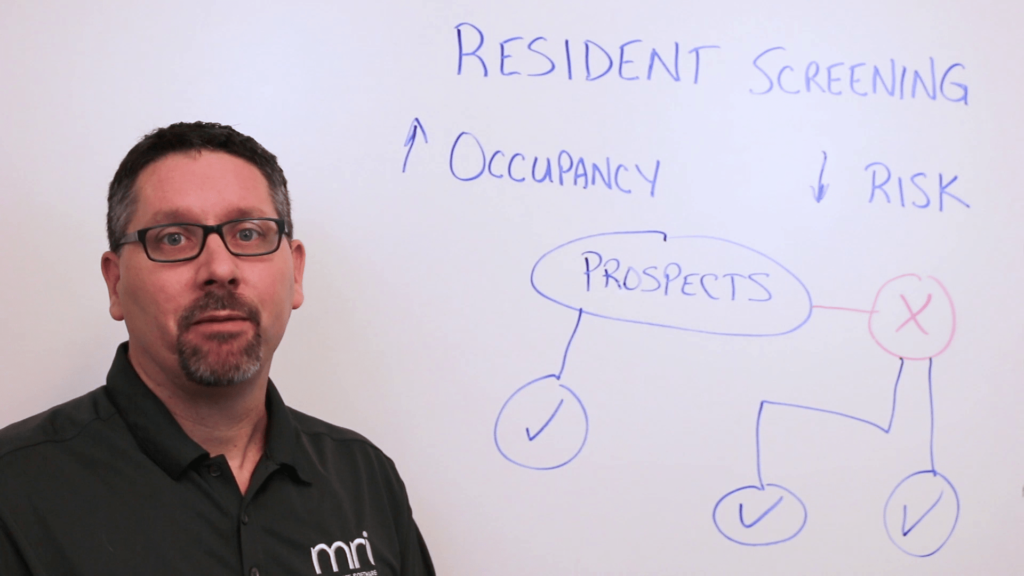

Andy Welkley: Hi, and welcome to this week’s edition of Whiteboard Wednesday. My name is Andy Welkley and I’m a product marketing manager here at MRI Software. Today, we’re going to talk about resident screening, that part of the application process that we tell our prospects is just a formality but we know can derail a lot of applications. Before we get started talking about the process, let’s talk why we do resident screening. Our goal as a leasing manager or a property manager is kind of twofold and really a balancing act. First, we’re charged with driving occupancy rates as high as we can, but at the same time we have to manage or mitigate the risk of bringing in residents who can cause problems, have delinquencies or late payments.

We’re really caught between two areas. How do we balance this? Well, resident screening is really the method that we use and most of the organizations that we work with use two sources to do this. First, they look at the FICO score or the credit score and they pair that with the criminal background check. That can lead to finding out of our pool of prospects, a group who we approve. That’s great. We’ve taken our prospects to the next level. We have a high degree of confidence that they’re going to balance this occupancy and risk category. What about the people who we deny?

There are certainly a group of those people who for whatever reason don’t have the credit score or the criminal background check that we identified as the threshold to balance the occupancy rates versus the risk. The problem with this method is that the FICO score is a very general measurement of overall financial health. It doesn’t zero in on resident specific behaviors or resident specific financial measures. Here at MRI we’ve developed our own model called the AccuScore which tries to do this. We zero in on things that are indicators of residential performance, the ability to pay rent, the ability to pay rent on time.

So, what we’re able to do is open up this pool of people who may have been denied from the FICO score and bring them down and approve them, still with the high degree of confidence that we’re mitigating that risk. At the same time we also know the people have criminal background checks that are full of errors. These background checks are generally conducted digitally and the databases contain errors, people with similar names or other issues that can cause a denial. We have a team of in-house investigators here at MRI that in person reviews these background checks, actually through a network, goes the steps of the courthouse to make sure that these are as accurate as possible.

Now, we have another source of approvals. We’ve taken this pool of prospects that were somewhat limited by our traditional methods and opened it up, driving the potential for our occupancy rates to increase. Well, at the same time, we’re not losing that element of mitigating risk. All this is very important to the process. You have the ability to customize that AccuScore to help understand what level of risk tolerance you have by property or even property type. If you have a traditional residential neighborhood or community, that’s fine, affordable housing, all those levers can be pulled to address this risk.

Now, at the same time you’re collecting a great amount of data here. We preserve that data so that you can actually drill down into each individual approval or denial and at the same time report on a whole host of these issues. You can evaluate this risk over time and optimize the whole system so that you are putting that in balance, driving occupancy rates as high as you can while at the same time mitigating risk. It’s a powerful tool to help you do your job even better and drive revenue to your property. That’s it for today’s Whiteboard Wednesday. I’m Andy Welkley. Thanks very much and we’ll see you again soon.